A budget is simply a tool for managing your income and expenses, but the method you choose makes all the difference. While the objective remains the same—to ensure you spend less than you earn—the strategies to get there vary widely. We’ve compiled a rundown of the primary budgeting types, including the popular Pay Yourself First method that prioritizes savings and the granular detail of Activity-Based Budgeting. Understanding these options is the first step toward tailoring a financial plan that truly works for you.

1. What Exactly is a Budget?

At its most basic, a budget is simply a financial roadmap or an educated guess about where your money will go over a specific period.

Think of it this way: instead of letting your money decide where it wants to wander off to each month, a budget lets you assign every rupee, dollar, or euro a specific job before the month even begins.

A budget is built on two main components:

- Income: All the money you expect to receive (like your salary, business profits, or investment returns).

- Expenses: All the money you plan to spend (like rent, groceries, debt payments, and savings contributions).

The goal is to ensure that when you subtract your expenses from your income, you are left with zero or a positive number. If you’re consistently spending more than you earn, your budget instantly highlights the problem so you can fix it.

2. Why is Budget Maintenance So Important?

A budget isn’t a one-time chore; it’s an ongoing process you need to maintain. Why put in the consistent effort? Because budget maintenance is what gives you financial control and peace of mind.

Here are the core reasons budget maintenance is crucial:

- Identifies “Money Leaks”: When you consistently track where your money goes, you quickly find those forgotten subscription fees, impulse buys, or the daily coffee habit that’s secretly draining your account. This awareness is step one to saving!

- Allows for Proactive Decisions: Without a budget, you react to bills and emergencies. With one, you proactively plan for big expenses (like car insurance premiums or holiday gifts) so you aren’t hit with a sudden financial shock.

- Manages Debt Effectively: Consistent budgeting ensures you always have enough to cover minimum debt payments, and even better, it helps you find extra money to aggressively pay down high-interest loans faster.

- Reduces Financial Stress: When you know exactly what you can spend and that your bills are covered, you avoid that constant worry about money. Spending becomes guilt-free because it’s already planned for.

3. What is the Core Purpose of a Budget?

The ultimate purpose of budgeting goes beyond just tracking numbers; it’s about aligning your spending with your values and goals.

- Achieving Specific Goals: Whether you want to save for a home down payment, fund a retirement account, or travel the world, a budget is the tool that turns that dream into a concrete, achievable plan. It dictates how much you must save each month to hit your target.

- Resource Allocation: For businesses and individuals, the budget is a blueprint for using scarce resources (money) in the most effective way. It forces you to prioritize. Do you value an expensive car payment or an earlier retirement? The budget helps you choose.

- Performance Measurement: It serves as a benchmark. At the end of the month, you compare your actual spending to your budgeted spending. This variance analysis lets you know if you are on track and helps you adjust your behavior for the next period.

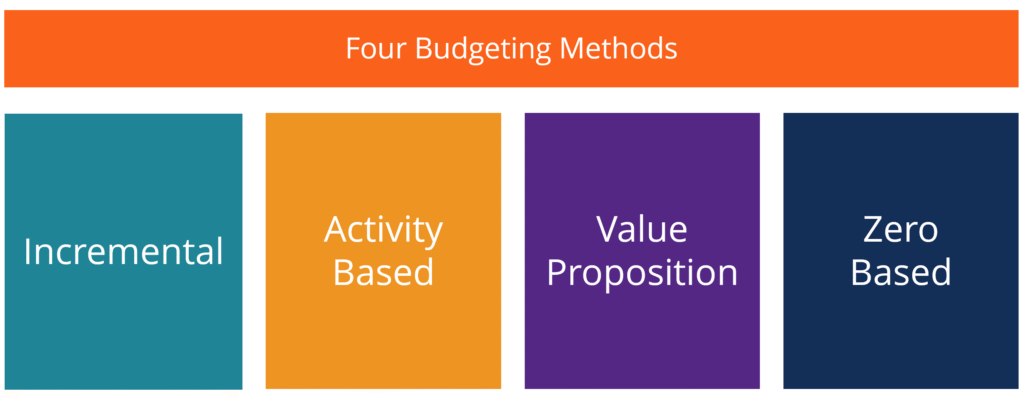

4. Key Types of Budgeting Methods

There isn’t a one-size-fits-all budget. Different methods work best for different people (or companies) based on their income stability and preferences.

| Budget Type | How It Works | Best For… |

| 50/30/20 Rule | Divides your after-tax income into three categories: 50% for Needs (rent, utilities), 30% for Wants (hobbies, dining out), and 20% for Savings/Debt Repayment. | Beginners who need a simple, high-level framework that balances living for today with saving for tomorrow. |

| Zero-Based Budgeting (ZBB) | Assigns every single unit of income a job so that: Income – Expenses – Savings = $0. It requires high discipline and tracking. | Anyone who feels like their money disappears every month. It’s excellent for debt repayment and maximizing every dollar. |

| Envelope/Cash Budgeting | Physically divides cash into envelopes for variable expenses (like groceries or entertainment) to prevent overspending in those categories. | People who struggle with overspending on credit cards and prefer a tangible, visual method to control costs. |

| Incremental Budgeting (Business) | Adjusts the previous year’s budget up or down by a small percentage, usually to account for inflation or small growth. | Stable businesses or departments with predictable operations. |

| Zero-Based Budgeting (ZBB) (Business) | Every line item in the budget must be justified from scratch for each new period, regardless of whether it was funded last year. | Companies undergoing major changes or looking for significant cost-saving efficiencies. |

5. How Budgeting is Changing Today (The Modern Shift)

Budgeting has moved past paper ledgers and complicated spreadsheets. Modern technology and global trends have driven significant changes in both personal and business finance:

- The Rise of Automated Tools: Modern budgeting is heavily influenced by technology. Apps like YNAB, Mint, or even bank-linked software automatically categorize transactions, track spending in real-time, and create visual reports. This has made maintenance far easier and less tedious.

- Rolling Forecasts (The End of the Annual Budget): In the business world, and increasingly for savvy personal users, the traditional annual budget is seen as too rigid. The trend is moving toward rolling forecasts (or flexible budgets), where the plan is continually updated—for example, every quarter—to adapt to real-world changes, market volatility, or unexpected expenses.

- Focus on ‘Value’ over ‘Cost’: Newer methods, especially in the corporate world (like Value Proposition Budgeting), focus on ensuring that every expense adds measurable value to the organization or individual goals, rather than just cutting costs blindly.

- The Integration of AI: We are starting to see AI and machine learning integrated into finance tools. These systems analyze your past spending to give you better, more accurate predictions about future costs, helping you save more efficiently without needing to manually crunch numbers.

Personal Budgeting Methods

These methods are typically used by individuals or households to manage their money.

- 50/30/20 Rule:

- Concept: Divides your after-tax income into three fixed categories.

- Allocation:

- 50% for Needs (essential expenses like housing, utilities, groceries, minimum debt payments).

- 30% for Wants (non-essential expenses like dining out, entertainment, hobbies, new clothes).

- 20% for Savings and Debt Repayment (emergency fund, retirement contributions, extra debt payments).

- Best for: People who want a simple, balanced, and flexible guideline.

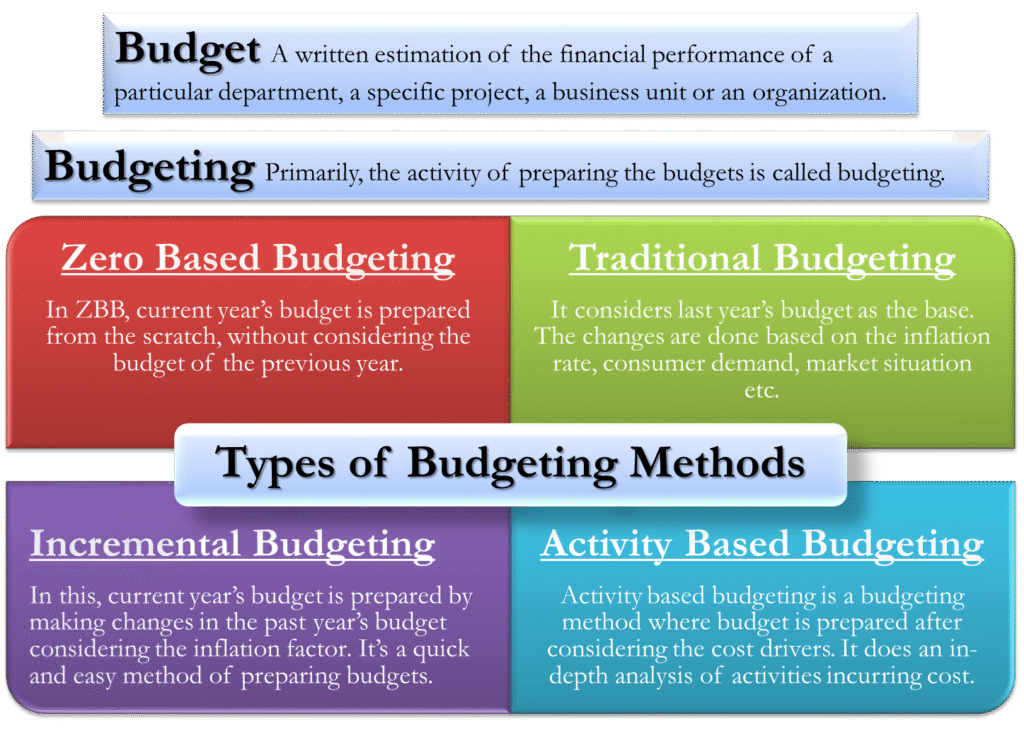

- Zero-Based Budgeting (ZBB):

- Concept: The goal is for your income minus your expenses to equal zero (Income−Expenses=$0). You assign a purpose to every dollar you earn.

- Process: You meticulously plan where every single dollar will go (to bills, savings, debt, or spending) before the month begins.

- Best for: People who need strict control, want to aggressively pay off debt, or want to maximize savings.

- Envelope Budgeting (Cash Stuffing):

- Concept: A system where you use physical (or digital) “envelopes” for variable spending categories.

- Process: At the start of the month, you put a set amount of cash into physical envelopes labeled for categories like groceries, entertainment, or gas. Once the cash in an envelope is gone, you can’t spend any more in that category until the next period.

- Best for: Visual or tactile learners, people who tend to overspend using credit/debit cards, or those who need a rigid spending limit.

- Pay Yourself First Budget:

- Concept: Prioritizes saving and investing by treating them as mandatory expenses.

- Process: As soon as you get paid, a predetermined amount is automatically transferred to your savings or investment accounts before you pay any bills or spend on wants. The rest of your income is then used for everything else.

- Best for: Prioritizing long-term financial goals and building a savings habit.

Business/Organizational Budgeting Methods

These methods are often used by companies or large organizations for operational and strategic planning.

- Incremental Budgeting (Traditional Budgeting):

- Concept: Creates the new budget by taking the previous period’s budget or actual results and simply adding or subtracting a small percentage (an increment) to account for inflation, anticipated growth, or minor changes.

- Pros: Simple, quick, and stable.

- Cons: Can perpetuate inefficiencies from the previous year and doesn’t encourage cost-cutting.

- Zero-Based Budgeting (ZBB):

- Concept: In a business context, this means all department budgets start at zero. Every expense must be justified and approved for the new period, regardless of whether it was included in the previous budget.

- Pros: Encourages managers to find more cost-efficient ways to operate and allocates resources based on current needs and objectives.

- Cons: Very time-consuming and labor-intensive due to the required detailed justification for every expense.

- Activity-Based Budgeting (ABB):

- Concept: Focuses on the cost of specific activities required to produce goods or services. It links spending directly to the activity that drives the cost.

- Process: Identifies the necessary activities, estimates the resources required for each activity, and then budgets the money needed to acquire those resources.

- Best for: Businesses that need a granular understanding of how resources are used and where inefficiencies exist.

- Flexible Budgeting:

- Concept: Creates a budget that can adjust automatically to changes in sales volume or other key metrics.

- Process: Rather than being based on a single, fixed level of activity, it provides different budget levels for different ranges of activity (e.g., if sales are high, the budget for materials and labor increases accordingly).

- Best for: Businesses with significant fluctuations in revenue or production volume.

#Budgeting #SmartBudgeting #MoneyManagement #PersonalFinance #FinancialFreedom #SavingMoney #BudgetTips #FinanceGoals #WealthBuilding #MoneyMatters #FinancialPlanning #Carrerbook#Anslation#MonthlyBudget #BudgetGoals #SpendWisely #MoneyMindset